The Real Cost of NOT Being on Quick Commerce in 2026

Not on quick commerce yet? Indian brands, including Blinkit and Zepto, are losing impulse sales, repeat customers, and first-mover positioning. Here's the real cost in 2026.

The consumer who ran out of your product last night didn't wait.

They opened Blinkit, found a competitor, and didn't think twice. That sale is gone. And if the competitor's product was good enough, which it probably was, your next three sales went with it.

This is the quiet cost of not being on quick commerce. Not a dramatic loss. A slow, invisible one. Order by order, replenishment cycle by replenishment cycle, while a competitor builds the habit loop you should be owning.

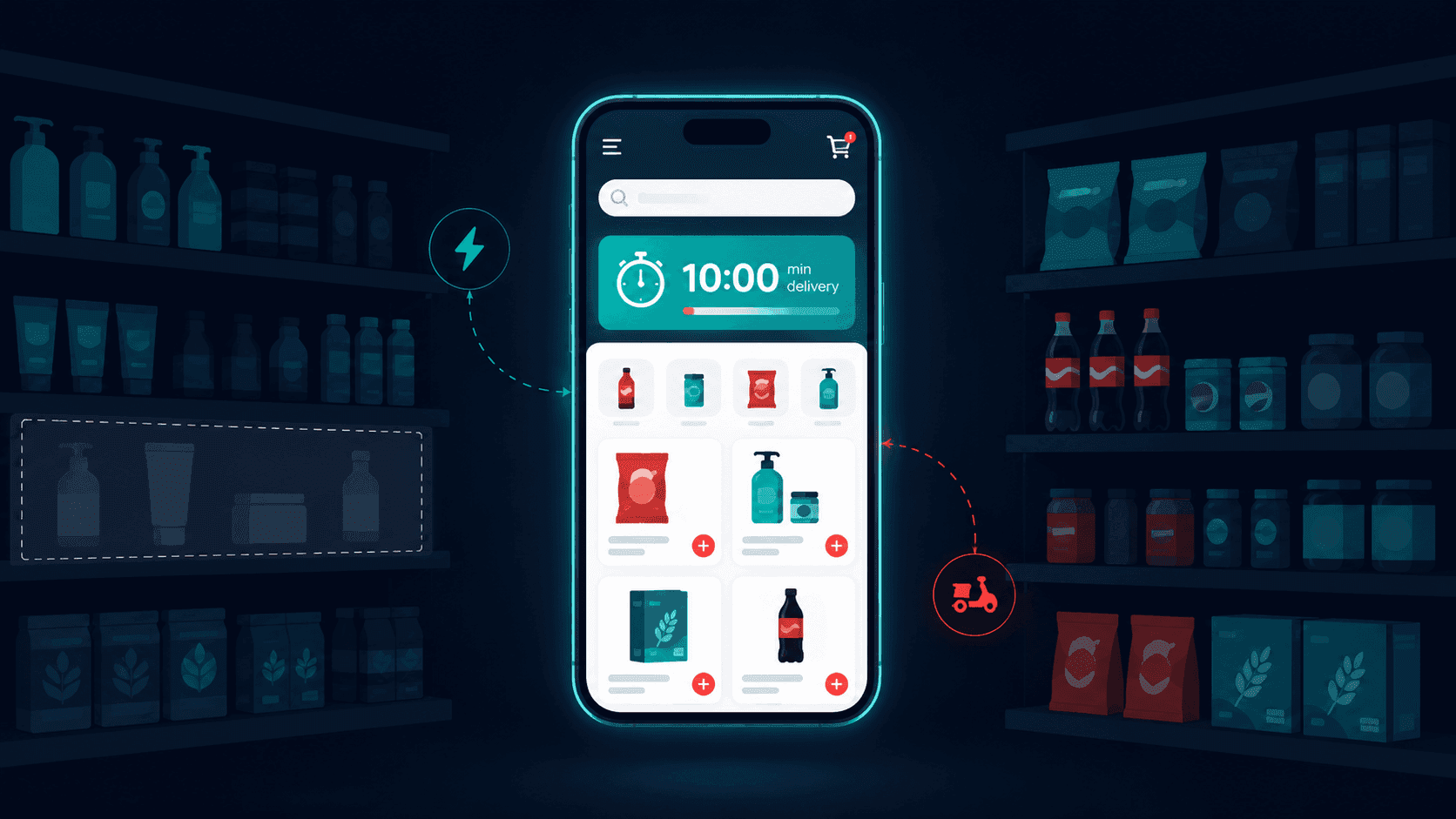

What Quick Commerce Actually Is in 2026

Quick commerce is no longer a novelty or a pandemic convenience. It is an infrastructure.

Blinkit operates 1,000+ dark stores across 50+ cities. Zepto expanded from 10 cities to 70+ in under two years and raised $350 million in 2024 at a $5 billion valuation.Swiggy Instamart is growing aggressively on the back of Swiggy's successful 2024 IPO and dominates South Indian and metro markets.

India's quick commerce market was valued at $3.34 billion in 2023 and is projected to reach $9.95 billion by 2029. That is a 22% CAGR, not the growth curve of a niche channel. That is the growth curve of a primary retail channel in formation.

The categories winning on Q-commerce have expanded well beyond grocery. Beauty and personal care are the fastest-growing non-grocery segments. Health and wellness, baby care, pet care, and electronics accessories are all seeing significant Q-commerce traction. The consumer behaviour shift that matters most: people are no longer using quick commerce only for emergencies. It is becoming their default channel for repeat purchase categories.

A brand not present on quick commerce is invisible during these purchase moments. Invisibility in a repeat-purchase channel is not a neutral position. It is a compounding loss.

The 5 Real Costs of Not Being on Quick Commerce

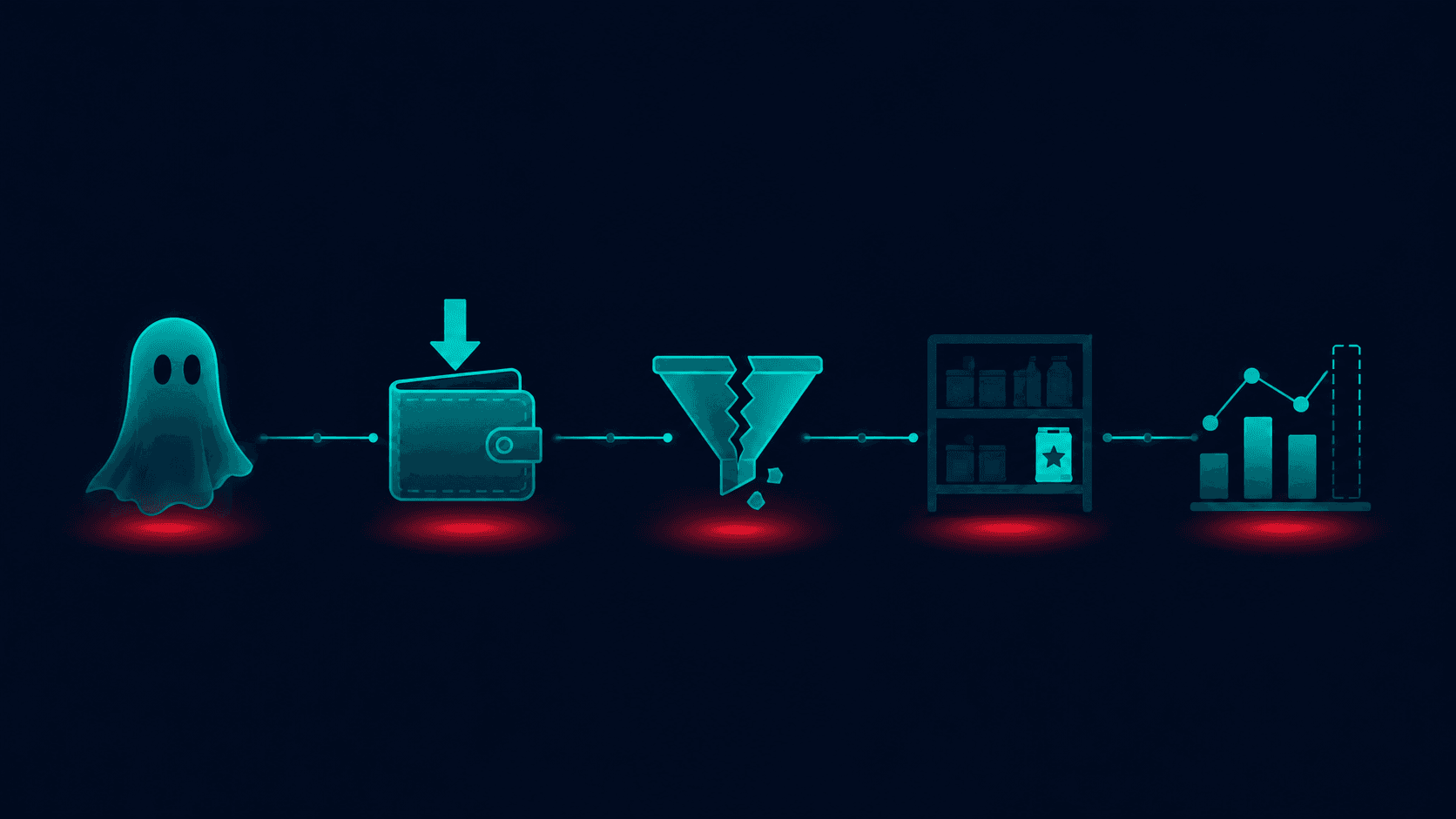

1. Impulse purchase invisibility

Quick commerce is structurally an impulse channel. A consumer who runs out of sunscreen at 8 pm doesn't open Amazon; the two-day delivery window doesn't solve a tonight problem. They open Blinkit. If your brand isn't there, a competitor's is. That purchase doesn't come back to you. And on a channel built on replenishment, the first brand that fills the gap owns the repeat.

2. Share of wallet erosion

Brands present on the quick commerce report that 30-40% of their q-commerce orders come from consumers who previously bought from them on other channels. These are your existing customers migrating to a faster, more convenient purchase moment, and if you're not on the platform, they're buying a competitor's version of your product instead. You are not just missing new customers. You are losing the ones you already had.

3. Discovery and new customer acquisition

Blinkit Ads and Zepto Ads are maturing into sophisticated performance marketing products, comparable to where Amazon Sponsored Products were two or three years ago. Brands running sponsored listings on quick commerce platforms are acquiring new customers through in-app search and category browse. Not being on the platform means missing this discovery funnel entirely, at the exact moment it is cheapest to win, before competition for ad inventory intensifies.

4. Dark store density as a competitive moat

Blinkit's 1,000+ dark stores represent physical retail infrastructure being built around Indian consumers right now. Brands listed on quick commerce are being embedded into that infrastructure, stocked in dark stores, factored into replenishment algorithms, surfaced in local search. Brands that wait will face higher competition for shelf space and potentially less favourable onboarding terms as platforms become more selective about who they stock.

5. Consumer data you are not collecting

Every quick commerce order is a real-time data point on purchase frequency, basket composition, geographic demand, and time-of-day patterns. Brands on q-commerce are building a consumer intelligence layer that informs everything from SKU planning to new product development. Brands not on it are making those decisions without the most current, granular signal available. In 2026, that is a meaningful competitive disadvantage.

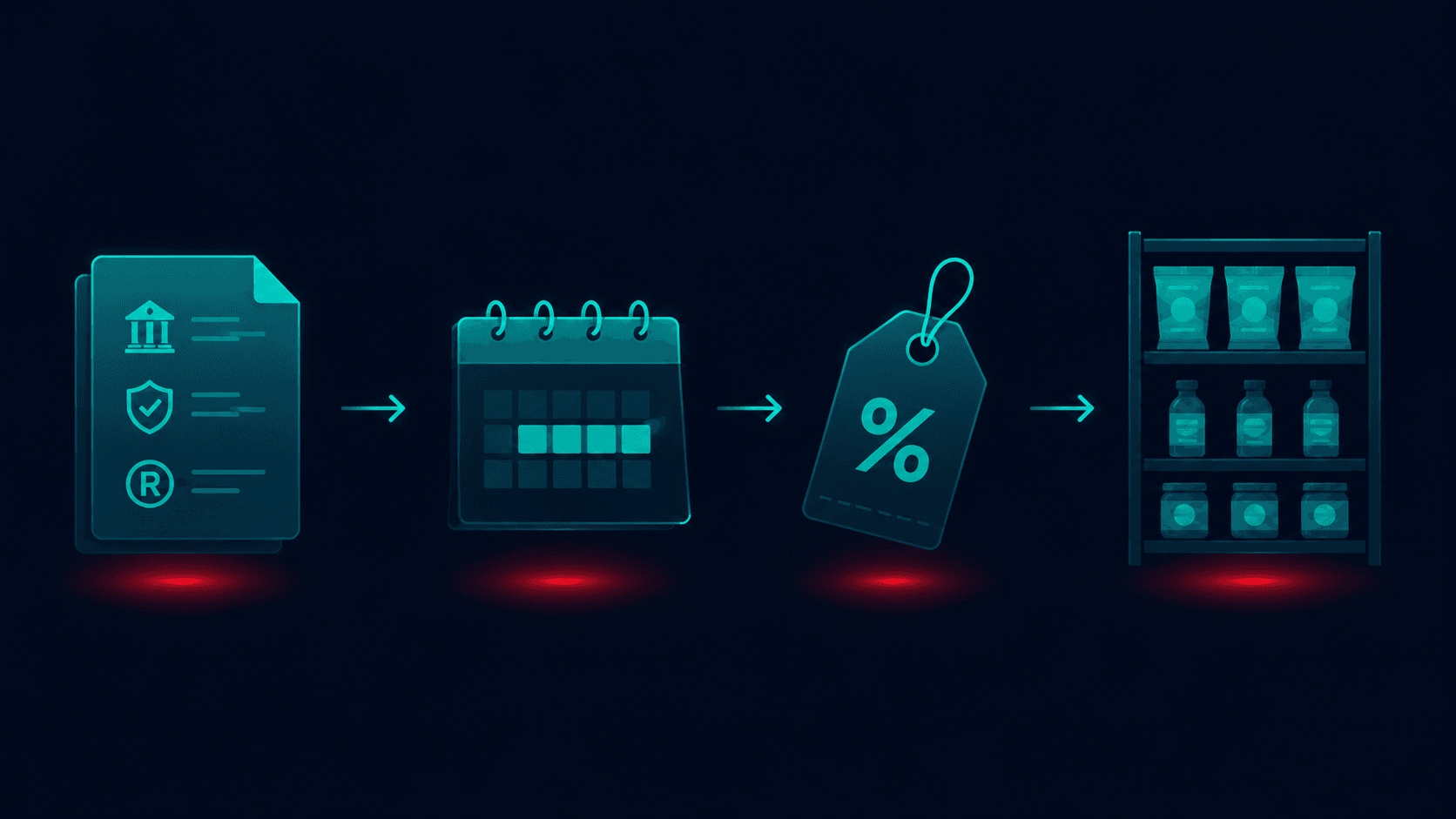

What Entry Actually Looks Like

The most common reason brands cite for not being on quick commerce is complexity. The reality is more manageable than most assume.

Documentation required: GST registration, brand trademark, and FSSAI license for food and personal care categories. These are documents most established brands already hold.

Timeline: Blinkit onboarding from application to first dark store stocking runs 4–8 weeks, depending on category. Zepto's Brand Partner programme has been actively fast-tracking D2C brands with proven Amazon or Flipkart traction; existing marketplace performance is an accelerant.

Commission structure: Quick commerce platforms take 15-25% commission depending on category, comparable to Amazon India rates. The unit economics conversation is real: average order values on q-commerce are lower than marketplace, so margin modelling per SKU matters before you onboard. Starting with 3–5 hero SKUs rather than your full catalogue is the right approach.

Inventory model: Dark store replenishment runs on smaller, more frequent cycles than warehouse-based marketplace fulfilment. Operationally, this is a different rhythm, one that rewards brands with flexible supply chains over those built for quarterly dispatch volumes.

The barrier to entry is not the platform. It is not knowing where to start.

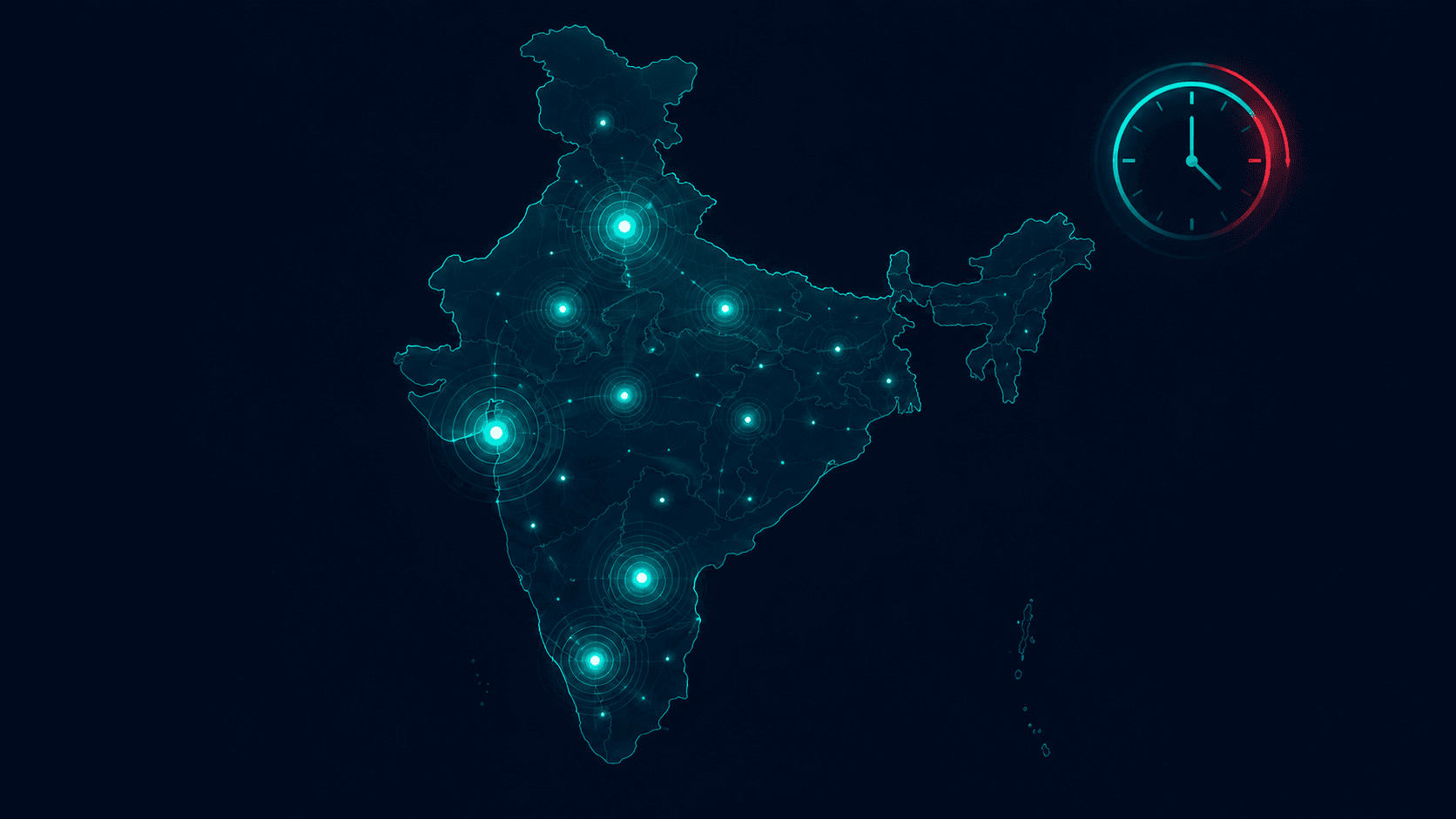

Why 2026 Is the Window and Why It Closes

Tier-2 expansion is happening now. Blinkit and Zepto are both aggressively entering cities beyond metros. Lucknow, Jaipur, Indore, Coimbatore, and Surat. Brands that onboard now gain first-mover positioning in these markets before competitors emerge. First-mover on a dark store shelf in a tier-2 city in 2026 is the equivalent of being an early Amazon seller in 2018.

Ad products are at the early-adopter inflexion point. Blinkit Ads and Zepto Ads are where Amazon PPC was before every seller understood it. Brands advertising on these platforms now are getting strong ROAS at lower CPCs. This window does not stay open, as more brands enter, ad competition increases, and early-mover advantage erodes.

Consumer habits are locking in. Every month that quick commerce is a consumer's primary replenishment channel, the behaviour becomes harder to dislodge. Brand presence during habit formation is disproportionately valuable, not just for the sale, but for the association. The brands that are there when the habit forms are the brands that get reordered automatically.

The cost of not being on quick commerce in 2026 is not what you're losing today. It is the market share, consumer habits, and dark-store positioning that your competitors are locking in while you decide.

Ready to Get Your Brand on Quick Commerce?

Pinnacle Growth Consulting offers a free Quick Commerce Onboarding Consultation, a clear-eyed assessment of which platforms fit your category, what your unit economics look like at q-commerce margins, and what the onboarding process actually involves for your brand.

No pitch. Just an honest look at whether quick commerce is the right move and exactly how to execute it if it is.